You want to improve your credit score to rent a house, secure a loan, or purchase a branded car. It’s exciting, isn’t it? However, high interest rates and strict credit limits can make the process frustrating. The worst part? Your loan application isn’t getting approved. A low credit score leads to fewer financial opportunities and higher borrowing costs.

As of 2024, the average FICO® Score in the United States stood at 715., indicating a generally positive credit health. Meanwhile, in India, the average credit score was also reported as 715. If you’re in a similar situation, don’t worry. In this article, we will share an effective approach to improving your credit score and helping you achieve better financial stability.

The best part? You don’t have to wait years. In just six months, you can see significant improvements in your credit score by following proven financial habits.

Quick Answer: How to Increase Your Credit Score Fast

To improve your credit score, adopt smart financial habits like making on-time payments, keeping your credit utilization low, and diversifying your credit mix. Avoid excessive spending and monitor your progress regularly using credit tracking tools like Experian Boost or Credit Karma.

Also Read:

- Indigo Airlines Case Study: From Runways to Soaring High

- The Future of Business: 15 Ideas You Need to Know for 2025

- Workday vs. Salesforce: Which One is Right for Your Business

Understanding Credit Scores: Why They Matter

A credit score is a numerical representation of a person’s financial trustworthiness, indicating their ability to manage debt responsibly. This three-digit figure helps lenders evaluate the risk of extending credit, influencing loan approvals and interest rates. It essentially reflects how trustworthy you are when it comes to borrowing money. Several factors, such as credit history, payment behavior, and credit utilization ratio, determine your credit score.

So, let’s assume you want a loan. The lender will assess your credit score to determine:

- Loan Application Approval

- Amount of Interest Rate

A higher credit score improves your chances of getting favorable loan terms, while a low credit score may lead to higher interest rates or even loan rejection.

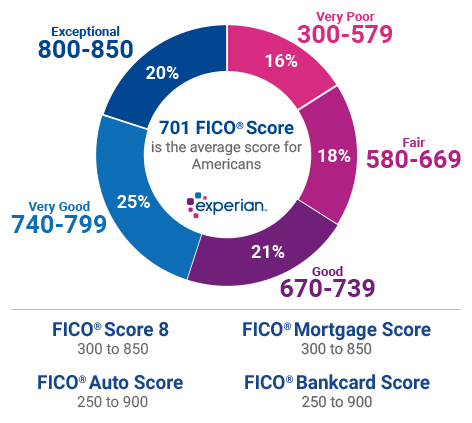

What is a good credit score?

A good credit score typically falls between 670 and 739 on the FICO® Score scale (300-850). Scores 740 and above are considered very good to excellent, increasing approval chances for loans and credit at better interest rates. Higher scores indicate responsible credit use, helping secure financial opportunities.

CIBIL Score vs. Credit Score: What’s the Difference?

Many people use CIBIL Score and Credit Score interchangeably, but they are not the same.

While all CIBIL scores are credit scores, not all credit scores are CIBIL scores

| FEATURE | CIBIL SCORE | CREDIT SCORE |

| Definition | A credit score issued by TransUnion CIBIL in India. | A general term for numerical scores used to assess creditworthiness globally. |

| Range | 300 – 900 | Typically 300 – 850 (varies by bureau). |

| Issued By | TransUnion CIBIL (India) | Multiple credit bureaus like Experian, Equifax, and TransUnion (Global). |

| Used For | Mainly considered by Indian lenders for loans and credit cards. | Used by banks, lenders, and financial institutions worldwide. |

💡 Key Takeaway:

- If you are in India, lenders will primarily check your CIBIL Score.

- If you are in the US or other countries, banks consider different credit scores from multiple credit bureaus.

Common Credit Scores: Significance

Your credit score impacts loan approvals, interest rates, and financial opportunities. Ranging from poor to excellent, it determines your borrowing power. A higher score means better loan terms, while a low score requires improvement for financial stability.

| Credit Score Ranges | ||

| Credit Score | Rating | Significance |

| 800-850 | Excellent | Best interest rates, good loan terms & lenders trust you |

| 740-799 | Very Good | Great loans deals & credit cards along with favorable terms |

| 670-739 | Good | Decent score. But improving it will lead to better offers |

| 580-669 | Fair | High interest rates, extremely strict lending requirements |

| 300-579 | Poor | Difficulty in approval, rebuilding score with right steps is needed |

6 Steps to Increase Your Credit Score in 6 Months

Before taking any action, you need to be clear about your current financial situation. Often, people check their credit scores without reviewing their official credit reports, which can lead to missed errors or outdated information. Here’s how to get an accurate view of your credit history.

Go to AnnualCreditReport.com—the only website that provides free credit reports from all major credit bureaus.

Check your reports from:

- Experian

- Equifax

- TransUnion

Once you have reviewed your credit reports, take note of any discrepancies, errors, or negative factors affecting your score. A proactive approach helps you tackle high-impact areas like credit utilization ratio, payment history, and outstanding debts—all of which influence your credit score significantly.

👉 Quick Summary: How to Improve Your Credit Score in 6 Months

- Check your credit report on AnnualCreditReport.com

- Keep your credit utilization below 30%

- Set up automatic bill payments to avoid late fees

- Dispute errors in your credit report

- Diversify your credit mix (cards, loans, etc.)

- Monitor your progress using credit tracking tools

Now that you have a clear understanding of where you stand, let’s explore the key steps to actively boost your credit score.

1. Minimize Credit Utilization Ratio

Did you know that credit utilization makes up 30% of your overall credit score? Keeping your credit usage low is essential, as it directly impacts your financial health and borrowing potential. Fixing it can provide an immediate boost to your credit health. To improve your score, ensure your credit usage stays below 30% at all times.

For example, if your credit limit is $10,000, your balance should never exceed $3,000. Here are some quick ways to lower your credit utilization:

- Request a higher credit limit, as an increased limit lowers your overall credit utilization ratio.

- Make additional payments before the statement date, reducing the reported balance and improving your score.

Maintaining low credit utilization signals responsible credit behavior, making you more attractive to lenders.

2. Don’t Delay Bill Payments

Approximately 35% of your credit score is determined by your payment history. Good financial habits of making timely bill payments crucial for maintaining a strong financial profile. Missing even a single payment can have a negative impact, leading to higher interest rates and lower creditworthiness.

To prevent late payments:

- Set up autopay to ensure bills are paid on time.

- If you miss a payment, contact your creditor and request a Goodwill Adjustment, which may remove the late mark from your credit report.

Lenders prefer consistent, on-time payments, so automating payments helps maintain a strong credit profile and prevents unnecessary penalties.

3. Identify Negative Items & Fix Credit Report Errors

According to Forbes, around 34% of consumers have noticed mistakes in their credit reports, which could be negatively impacting their credit score. Identifying and disputing these errors can help boost your credit score significantly.

Here’s my simple practical tips on “how to fix errors in your credit report”:

- Check for inaccuracies such as incorrect payment information, duplicate accounts, or outdated debts that should be removed.

- Make a detailed list of all discrepancies to ensure nothing is overlooked.

- Dispute errors online with Experian, Equifax, and TransUnion to correct inaccuracies and improve your credit standing.

Fixing errors not only helps increase your credit score but also ensures that lenders assess your financial credibility accurately.

4. Focus on Building Positive Credit Habits

Improving your credit score isn’t just about fixing mistakes. It more about adopting healthy financial habits that lead to long-term benefits.

One of the best ways to strengthen your credit profile is to diversify your credit mix. Lenders assess various forms of credit to gauge your creditworthiness, considering how well you manage different types of debt. Consider a combination of:

- Credit cards

- Installment loans (including auto loans and student loans)

- Credit builder loans

Another effective strategy is becoming an authorized user on someone else’s old credit card with a strong payment history.

How does this help?

- It enhances your credit history by adding years of responsible usage to your report.

- It improves your credit utilization ratio, making you look more reliable to lenders.

To maximize the benefits, ensure the account is at least five years old and has a solid history of on-time payments.

5. Always Keep Track of Your Credit Score Progress

Following these strategies is enough? No.

Improving your credit score is an ongoing process, and tracking your progress is essential for long-term financial health. Regular monitoring helps you detect fluctuations, potential errors, or areas needing improvement before they impact your score.

Use free credit monitoring tools such as:

These tools allow you to receive real-time credit alerts, track changes in your credit utilization ratio, and monitor payment history trends—all of which influence your creditworthiness.

- If things are going according to plan, continue following the same financial strategy.

- If your credit score isn’t increasing, reassess and restrategize to identify problem areas.

Pro Tip for Easy Tracking

Use Google Sheets to log your monthly balances, due dates, and credit score changes. Keeping a digital record helps you analyze patterns and adjust your financial habits proactively.

Also Read:

- Workplace Rights 101: Understanding Employee Rights & Employment Law

- Mastering Voice Search Optimization: A Comprehensive Guide

- Return on Ad Spend (ROAS): Boost Profits from Every Marketing Spent

FAQ: Improve Your Credit Score

How fast can you boost your credit score?

Improving your credit score can takeas little as six months with consistent on-time payments, low credit utilization, and disputing report errors. Using credit monitoring toolshelps track progress and adjust strategies as needed.

What impacts my credit score the most?

The biggest factors affecting your credit score are payment history (35%), credit utilization (30%), and length of credit history. Keeping balances low, making payments on time, and maintaining older accounts can significantly improve your credit standing.

Is it better to pay off debt or increase my credit limit?

Both help improve your credit score. Paying off debt lowers utilization, while a higher credit limit reduces your credit usage ratio. If possible, do both to strengthen your financial profile and improve loan eligibility.

Final Thoughts: Boost Your Credit Score in Just 6 Months

Improving your credit score in six months isn’t impossible. We have shared proven financial strategies, and if you stay consistent, you’ll see visible improvements in your credit profile.

To maintain a healthy credit score, remember:

- Keep your credit utilization rate below 30% to optimize your creditworthiness.

- Avoid late payments—delayed bills can pile up and lead to financial difficulties.

- Automate bill payments to ensure on-time payments and prevent penalties.

This approach not only helps with a faster credit score increase but also builds long-term healthy financial habits.

Take Action Today By following these steps, you can achieve a stronger financial position in just six months.

Have More Questions? If you have any questions, don’t hesitate to ask. How much time does it take to raise a credit score? What are the most effective ways to repair bad credit? Leave your questions in the comment section, and our team of experts will get back to you as soon as possible.

Share your Review

Revise and Edit by Editorial Team

Connect with us on our Digital Endeavours-

Transforming Lives… Creating the magic. Just – Believe ~ Practice ~ Perform

BizTech Chronicle… Navigating Tomorrow’s Tech Frontiers 🚀

Youtube – Nuteq Entertainment Pvt Ltd

Trendvisionz – A Premier Digital Marketing Agency in India

Follow me on Twitter or LinkedIn. Check out our website.

1 comment

This blog provides a practical step-by-step guide to improving your credit score in six months. A must-read for anyone looking to boost financial health and secure better loan opportunities!

Comments are closed.